It’s easy to think of supply chain resilience as something that only concerns large corporations with complex global logistics. In reality, every growing business that sells on credit terms is exposed to supply chain risk — because when a customer doesn’t pay, the disruption doesn’t stop with you. It travels down the chain to your own suppliers, your staff, and your ability to take on new work.

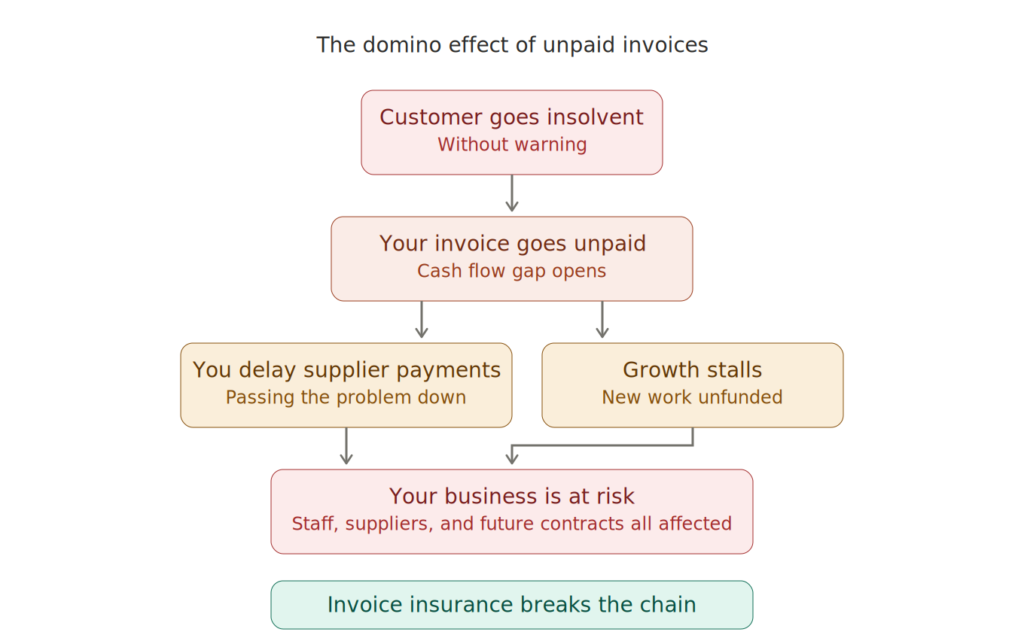

The domino effect is real

When a customer becomes insolvent or simply refuses to pay, the immediate impact is obvious: you’re out of pocket. But the knock-on effects are what catch businesses off guard. You may need to delay payments to your own suppliers. You might have to hold off on hiring, pause a project, or turn down new business because you can’t fund it. In the worst cases, a single large unpaid invoice can push an otherwise healthy company to the brink.

This isn’t theoretical. UK corporate insolvencies hit nearly 24,000 in 2025, and remain well above pre-pandemic levels heading into 2026. Construction, wholesale, and manufacturing have been hit hardest — sectors where businesses routinely extend credit to customers and operate on tight margins. When one firm in the chain goes under, the unpaid invoices it leaves behind can trigger a cascade of financial stress for every business connected to it.

A single customer’s insolvency can harm your business. Invoice insurance prevents that harm.

Late payment is getting worse, not better

The broader trend makes uncomfortable reading for any business that trades on credit. UK SMEs are now owed an average of nearly £67,000 in unpaid invoices, and around 62% report that their customers are taking longer to pay than a year ago. A House of Commons report put the total figure owed to SMEs at £112 billion.

What’s particularly concerning is the shift from late payment to outright bad debt. Nearly a third of businesses have written off an average of £30,000 over the past year due to customer insolvency or default. That’s not a cash flow inconvenience — it’s a direct hit to profitability and a serious threat to business continuity.

Rising energy costs, higher employer National Insurance contributions, and a slowing economy are all adding pressure. When your customers are under financial strain, their problems become your problems — often without warning.

Unpaid invoices and slow repayments put UK SMEs at significant risk.

What resilience actually looks like

True supply chain resilience isn’t just about diversifying your suppliers or holding more stock. It’s about protecting your revenue from the risks you can’t control. You can’t stop a customer from going insolvent. You can’t force them to pay on time. But you can make sure that when things go wrong, your business doesn’t go down with them.

That’s what invoice insurance is designed to do. It protects your business against both insolvency and protracted default from your customers, ensuring you get paid for the work you’ve done regardless of what happens at the other end.

With a policy in place, you’re not left chasing debts or writing off losses. You can continue paying your own suppliers, keep your staff employed, and maintain the cash flow you need to operate and grow. It removes the uncertainty that sits at the heart of every trade credit relationship.

Prevention, not reaction

The businesses that come through difficult economic periods tend to be the ones that planned ahead. Waiting until a customer goes under to think about protection is too late — the money is already gone.

Invoice insurance works best when it’s in place before problems arise. It gives you the confidence to extend credit terms, take on new customers, and pursue growth opportunities, knowing that your invoices are protected.

In the current climate, with insolvencies elevated and payment times stretching, that kind of certainty isn’t a luxury. It’s a practical necessity.

Links (these open in new tabs)

Invoice Insure Homepage

Invoice Insure Articles

Assured Trade Homepage

Assured Trade LinkedIn