Three centuries ago, a financial mania nearly destroyed Britain. Today, the same thinking deceives the world. This is the story of the South Sea Bubble, its dystopian aftershock, and what businesses can do to avoid false lures of glitter and gold.

“Whole communities suddenly fix their minds upon one object, and go mad in its pursuit; that millions of people become simultaneously impressed with one delusion, and run after it, till their attention is caught by some new folly more captivating than the first.” Charles Mackay, Memoirs of Extraordinary Popular Delusions and the Madness of Crowds, 1841.

Britain Sunk

By the end of 1720, Great Britain was on the verge of ruin. Rioters burned towns. Anger, misery and doomsday prophecies spread. People were hanged in the streets. Thousands committed suicide or fled to mainland Europe. Others became indentured servants, slaves in all but name, and worked without pay for the rest of their lives. Banks and hundreds of traders, guilds, and small firms failed. Lords, Earls, Barons, and other peers, noblemen and landed gentry were bankrupted, dispossessed of assets, killed themselves, or died in penury.

The Kingdom, formed just 13 years earlier when England united with Scotland, was about to topple. A First Lord of the Treasury, a Chancellor of the Exchequer, a Postmaster General, and a Secretary of State were bankrupted, impeached, imprisoned, killed themselves, fled, or died in penniless shame. Even the King lost money.

The South Sea Bubble had burst.

“Britain,” wrote Alexander Pope, who lived through the era, was “sunk in lucre’s sordid charms.”

Half a year before, nobody had predicted the devastation.

Wisdom Stoops to Folly

In May 1720, investment fever gripped the United Kingdom. Peasants and young women prostituted themselves to buy shares. Men sold their homes, their properties and anything of value to raise money.

Investors flock to Cornhill Street in 1720 at the height of the South Sea Bubble.

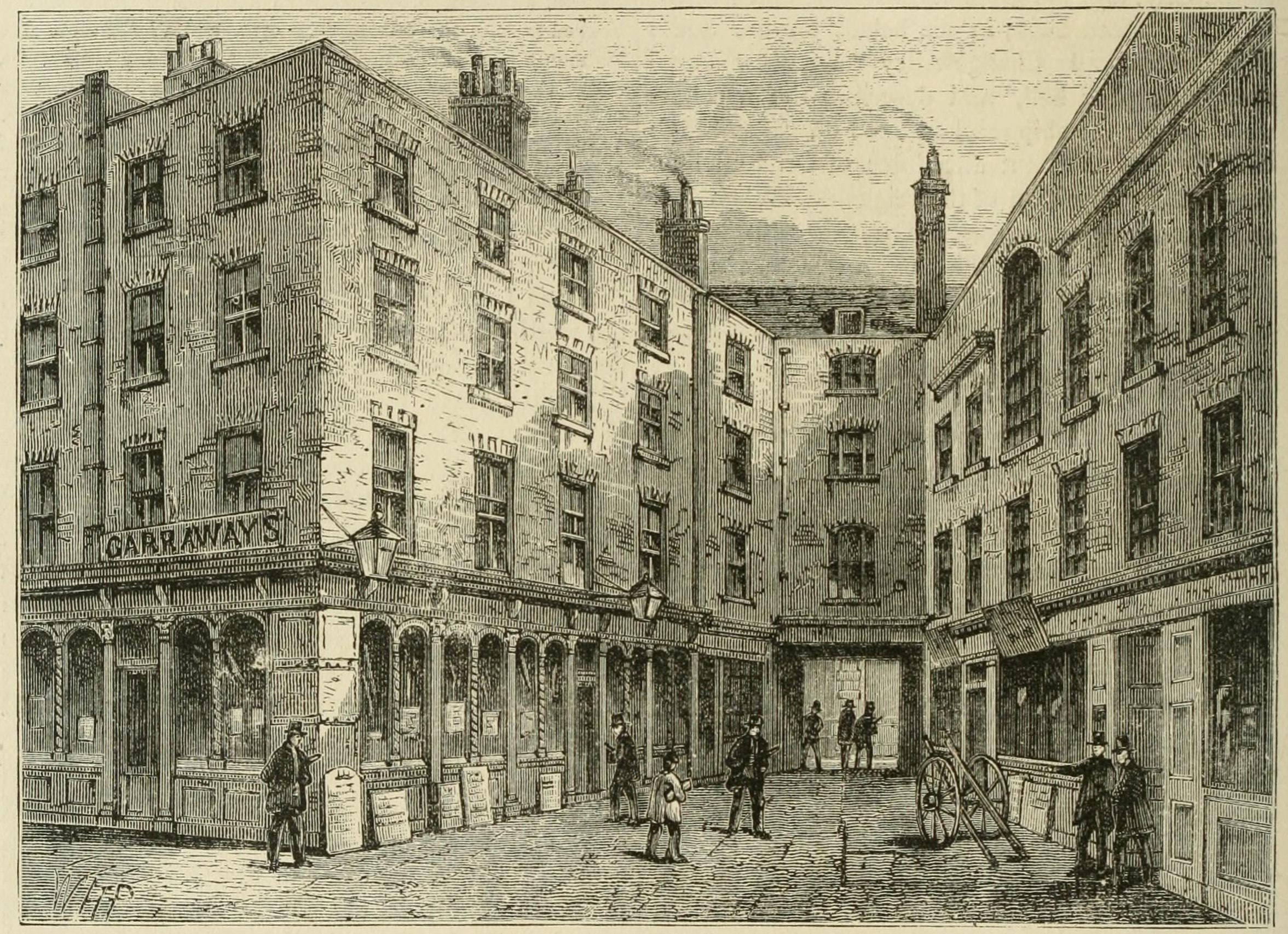

The old and the young, the rich and the poor, craving gain, became speculators. Buying stocks seemed the way to wealth. Every day, carriages clogged Cornhill Street. Investors crammed into Garraway’s Coffee-House and Jonathan’s Coffee House, both on Change Alley.

Garraway’s Coffee House, a central hub of speculation during the South Sea Bubble of 1720.

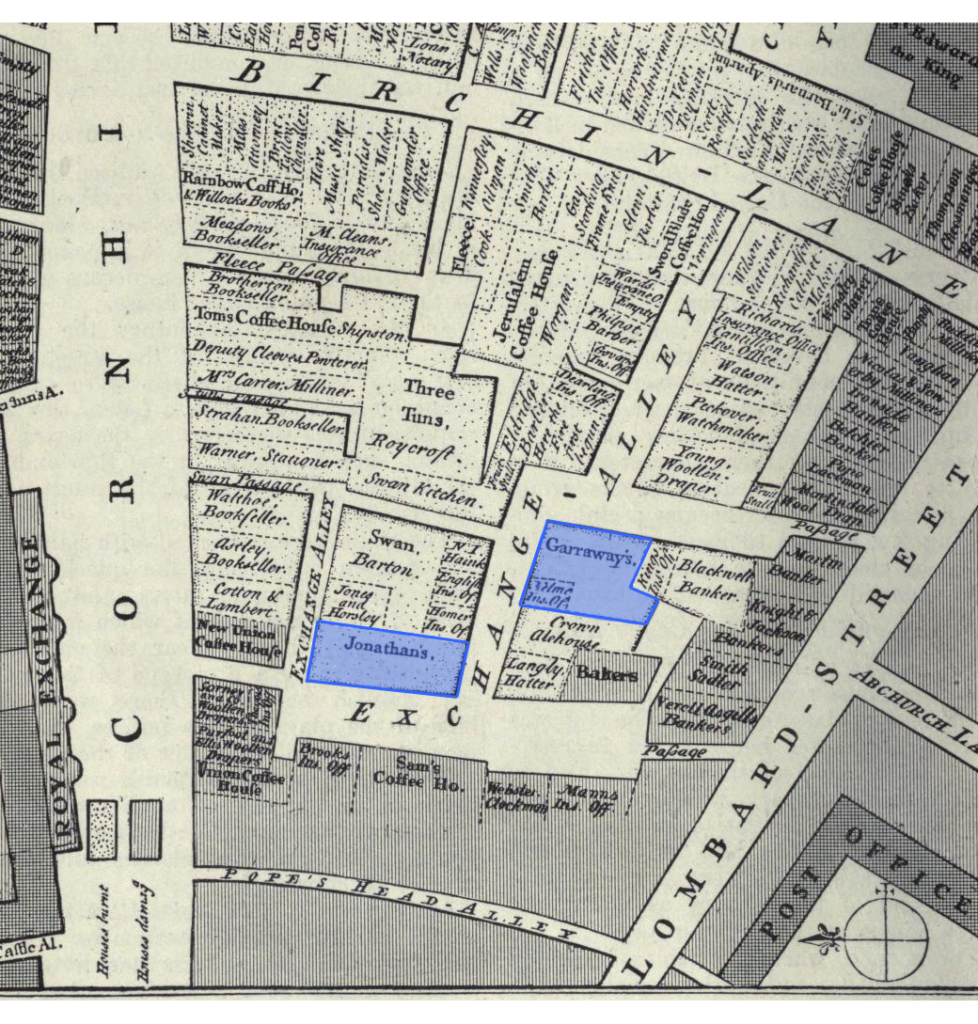

All of this happened in an area smaller than a football field, across the street from what is today the Royal Exchange. Stockbrokers had been banned from the Exchange years earlier because of their rowdiness and poor manners.

Map of Cornhill, specifically Change Alley. Garraway’s and Jonathan’s Coffee Houses are highlighted in blue. There, stock trading occurred in the 1700s. Stockbrokers had been banned from the Royal Exchange, which sat then where it does today, to the west of Change Alley across Cornhill Street.

Shareholders sold everywhere else, too, from open squares to public houses. Hawkers knocked on doors. Others printed pamphlets publicising the shares and the scheme upon which the South Sea Company had been founded.

The Origins of the South Sea Scheme

The South Sea Company was founded in 1711. Costly wars caused Britain’s debt to reach alarming levels. Only two companies—the East India Company and the Bank of England—were permitted to lend the government money.

The Dividend Hall of the South Sea House at the intersection of Bishopsgate and Threadneedle Streets, where the infamous scheme was conceived.

The South Sea Company was designed to offer a third solution: a private entity that would manage part of the national debt while promising lucrative trade opportunities.

Spain and Portugal controlled merchant trade between Europe, Africa and the Americas. Untapped riches lay there, across what people called the South Seas. But at war with Britain, Spain prevented British merchant ships from accessing their American colonies.

Robert Harley and John Blunt were the two figures at the heart of the South Sea Company’s creation.

Harley, who’d served as the Speaker of the House of Commons under Queen Anne, was, by 1711, the Chancellor of the Exchequer and chief of the Queen’s ministers. A Tory, he was a lifelong opponent of Robert Walpole, the influential Whig and forceful speaker who’d later assume the same positions Harley enjoyed. Harley first tried bringing Walpole to the Tories. Unsuccessful, he induced Walpole’s impeachment under charges of corruption. Expelled from Parliament, Walpole spent half a year in the Tower of London. Walpole would get his revenge. Meanwhile, Harley aimed to use the South Sea Company to compete with the Whig-controlled Bank of England.

Robert Harley, 1st Earl of Oxford, an architect of the South Sea Company and prominent figure in early 18th-century British politics. (Source: The National Portrait Gallery.)

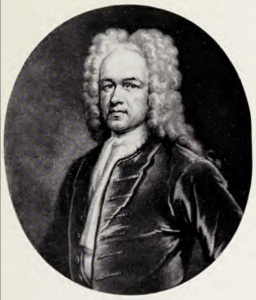

John Blunt’s motives were less political and more personal. A commoner, he wanted the South Sea Company to be Britain’s third great economic institution, bringing him and the others involved power and wealth. Failing that, he’d pump the stock price high enough for insiders to exit with substantial personal gains. Blunt understood that the Company’s real success would lie more in speculation and marketing than trade.

Sir John Blunt, a central figure in the creation and rise of the South Sea Company.

Thanks to Harley, who’d long been close to Queen Anne, the South Sea Company received a monopoly on trading with Spain after the war ended — as most assumed it soon would. Harley encouraged peace, partly because he knew it would allow trade and enhance his fortune, and partly because the war was sending Britain into greater debt. Armies on the continent hadn’t enough to pay, clothe and feed their soldiers. The Queen’s approval gave legitimacy to the venture.

Having received royal assent, the South Sea Company offered to assume £10 million of government debt, more than 15% of the national GDP, with debt holders able to exchange their government bonds for South Sea Company shares. The Tory parliament, inspired mainly by Robert Harley, approved the proposition. Since it promised an orderly means of consolidating the nation’s finances, the proposal appealed to creditors and officials alike.

In 1713, the war ended under the terms of the Treaty of Utrecht. The Treaty’s terms were unfavourable and caused a furore that would soon lead to Harley’s downfall. It allowed only one British ship per year to engage in general commerce, subject to heavy taxation by Spanish authorities. The goal of unrestricted trade was gone.

Pages from the Treaty of Utrecht (1713). Its terms shaped the trading conditions underpinning the South Sea Company and led to Robert Harley’s demise.

Despite these constraints, the South Sea Company traded slaves. It wasn’t a Ponzi scheme from the start. The Company skirted the Treaty’s terms and often refused the Spanish Empire’s demands, trading illegally. The result was a poor relationship with the Spanish, which meant their trade was consistently unprofitable.

After the Treaty of Utrecht, the Company’s share price fell, but didn’t curtail investment as severely as expected. Politicians, financiers, the Company’s members and the press all worked to sustain a positive view of the enterprise. By offering to place clerics aboard each merchant ship and disclosing an apparently upright, well-regulated system of operations, the South Sea Company presented itself as virtuous and dependable.

An engraving glorifying the South Sea Company, emphasising its promise of prosperity and national trade dominance.

In 1714 Queen Anne died. King George I acceded to the throne. In 1715, the Whigs regained control of the government. Robert Harley lost his ministerial position. Because he’d helped negotiate the Treaty of Utrecht, Whigs blamed him for its unfavourable terms.

The Whigs reinstated Robert Walpole into Parliament and impeached Harley for high treason. While awaiting trial, he was imprisoned in the Tower of London. After two years, he was released and acquitted. His health deteriorated during his detention. King George banished him from the royal court. Even though he resigned from politics after his acquittal, his early involvement with the South Sea Company wasn’t forgotten.

The Whigs reformed the South Sea Company’s board. John Blunt retained his role and cultivated connections throughout government and society. Unbound by politics, Blunt’s genius lay less in sound business sense and more in his ability to sell the promise of wealth.

Public confidence in the Company soared when King George I became one of its directors in 1718. His son, the future King George II, also joined the board. Royal eminence boosted the stock price, and the South Sea Bubble expanded quickly thereafter.

A Plague of Frauds: The Bubble Companies

Halfway through 1720, the South Sea Company’s wealth attained new heights. A slew of imitative companies surfaced, and with them, more bubbles appeared. The crowds packed Change Alley in numbers never before seen.

Outdoor trading in Change Alley, depicted in Edward Matthew Ward’s 1847 painting, showing the chaos and fervour of the time.

Founded by charlatans, these companies advertised the most ridiculous products. In the words of the Encyclopaedia Britannica, the great majority “put forward the most audacious and chimerical proposals for extracting money from the public.”

One of them promoted “a wheel for perpetual motion”. It raised a million pounds (about £188 million today).

Another said it would encourage “the breed of horses in England, and improving of […] church lands, and repairing and rebuilding parsonage and vicarage houses.” The company never explained why the church would be interested in breeding horses. The firm sold shares quickly.

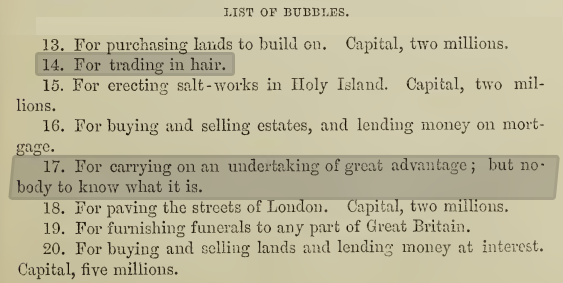

Nearly a hundred such companies existed in 1719. A few examples follow, later declared illegal and abolished:

– A company for “trading in hair”.

– A company for “extracting silver from lead”.

– A company for “purchasing and improving a manor and royalty in Essex”.

– A company for “a grand dispensary”.

– A company for “purchasing lands to build on”.

Just a few of the bubble companies from 1719 and 1720, highlighting absurd ventures such as ‘trading in hair’ and ‘carrying on an undertaking of great advantage, but nobody to know what it is’.

The shortest-lived, although by no means the most cynical of these companies, was one that proclaimed a “design which will hereafter be promulgated.” The entrepreneur called it ‘A company for carrying on an undertaking of great advantage, but nobody to know what it is.’

Charles Mackay, a Scottish poet and journalist, wrote an 1841 book, Memoirs of Extraordinary Popular Delusions and the Madness of Crowds. He called the mysterious company an “inroad upon public credulity”.

The day after advertising the company’s foundation, the opportunistic originator opened an office on Cornhill Street. Throngs crowded his door. In five hours, he sold a thousand shares. He made £2000 (equivalent to about £380,000 today). Content with his proceeds, he made for the continent that night. He wasn’t heard from again.

Desperate buyers in Change Alley.

This trickster had exploited the mania of the times. But his appeal to secrecy, as though he’d originated some mechanism so ingenious that its details could not be revealed, is not substantially different from the appeal that Enron had, the appeal that FTX had, the appeal that many cryptocurrencies have and the appeal that too many companies today have, and use.

Voices of Warning

A few judicious people warned against the South Sea Bubble and its imitators. In his book, Mackay praised Robert Walpole for his speeches in the House of Commons, in which Walpole condemned the folly of South Sea Bubble investment. Like some of his family members and political consorts, Walpole had invested in the Company. Astute enough to know when to sell, he reaped a 1000% profit. Hypocritical though his actions may have been, his denunciations were eloquent.

Robert Walpole, Whig powerbroker and orator, he is today considered Britain’s first Prime Minister, thanks largely to his management of the South Sea Bubble’s aftermath.

In one speech, Walpole warned that the South Sea Company would “divert the genius of the nation from trade and industry.” It would, he said, “hold out a dangerous lure to decoy the unwary to their ruin, by making them part with the earnings of their labour for a prospect of imaginary wealth.” If the scheme failed – at the time Walpole spoke those words, it had not – the consequences would wreck the nation. “Such would be the delusion, that when the evil day came, as come it would, the people would start up, as from a dream, and ask themselves if these things could have been true”. His words went unheeded. Parliamentarians saw only “visions of ingots”.

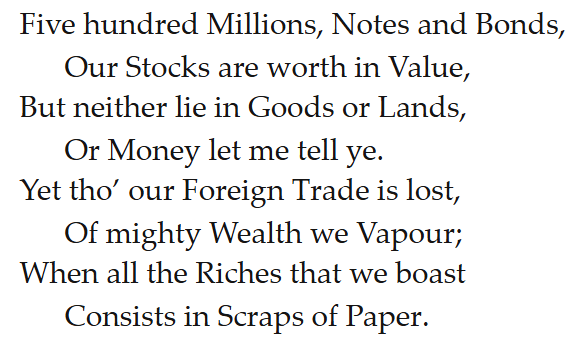

A 1720 doggerel by Ned Ward was more scathing.

A stanza from Ned Ward’s comic verse, ‘A South-Sea Ballad, or, Merry Remarks upon Exchange-Alley Bubbles,’ satirising the consequences of the South Sea Bubble. (Source: Grub Street Project.)

Prophetic, the ballad thrived as the South Sea Bubble quivered and shook, contracted a bit, and further swelled.

A cardmaker published playing cards lampooning the South Sea Company and the short-lived, bogus companies whose foundation the South Sea Company’s success motivated. Some of the cards, now extremely rare, have been printed in Mackay’s book.

An extremely rare playing card lampooning the financial frenzy, it is entitled ‘The Humours of Change Alley’. (Image condensed and modified for readability and clarity.)

The Bubble Quivers, Shakes and Bursts

By the end of May 1720, Parliament accepted a second proposal by the South Sea Company, this time to assume the total national debt rather than just part of it. The Company’s directors were awarded titles. Harley was already an Earl. On 11 June 1720, King George made John Blunt a baronet.

Warrant for conferring the title of baronet upon John Blunt, signed by King George I on 19 July 1720. (Source: The National Archives.)

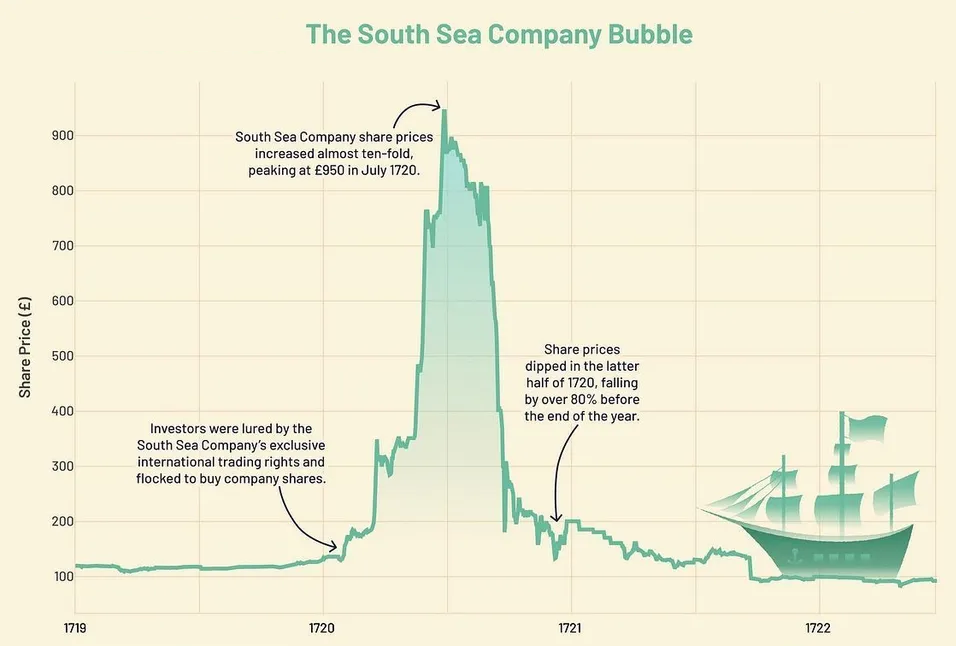

The shares reached 250%, 560%, then 680% of their original value. Some traders sold them in bundles or limited-time offers at 2000%. By August, the shares reached £950, then £1000 (or £188,800 today). Insiders started cashing out.

The South Sea Bubble quivered and shook. It was about to burst. Company insiders bought shares themselves as they tried to stop prices from sliding. They loaned money to investors, who, they hoped, would buy shares with that money. The plan failed when borrowers had to sell their shares to repay the loans.

The rise and fall of the South Sea Company’s share prices, showing the dramatic peak in July 1720 and the subsequent collapse. (Data sourced from the European State Finance Database, presented by Genuine Impact.)

This sort of bizarre trading came near to surreal. Blunt and the other schemers tried all sorts of similarly ridiculous contrivances to sustain the Company’s value. Calls for parliamentary scrutiny increased, although hundreds of parliamentarians were still then investors in the South Sea Company. A few made speeches defending the firm. More sold stocks and stayed quiet.

The realisation hit hard and fast: not even the most lucrative slave trading company could justify the share prices the South Sea Company had reached. The shares weren’t worth the gold, jewels, property and everything else investors had sold to buy them. Ink-scrabbled papers, the shares amounted to little more than IOUs.

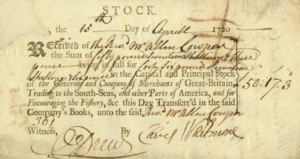

South Sea Company stock certificate dated 15 April 1720, representing a share of the South Sea Company’s speculative value during the height of the bubble.

The South Sea Company made no money via merchant trade. It had no sustainable income apart from its shares. In September, the share price tumbled.

The multitudes had fallen into a trap, cunningly laid. The result was calamitous, as has been earlier described. Late investors and those who’d borrowed heavily were ruined. People across the nation were penniless and ran, in the words of Charles Mackay, “to and fro in alarm and terror. [The] degrading lust of gain […] had swallowed up every nobler quality in the national character.” Quaking with fear, wanderers spoke of the apocalypse in the same terms their forefathers had during the Great Plague of 1655.

In London, the Bubble had expanded and broken. From there, too, it grew — like bubonic bacilli three generations before. Across the country, impoverished masses, enraged, retaliated where they could. In the most violent incidents, stock sellers were hanged, drawn and quartered. Bankers, goldsmiths and upstanding firms had lent large sums against the stock, and as prices fell, they failed.

Isaac Newton, who’d owned £22,000 worth of South Sea Company shares, which would be close to £4 million today, lost nearly all of it. “I can calculate the movement of the stars,” said Newton, “but not the madness of men.”

Bonfires, riots, and mobs at Tower Hill after the South Sea Bubble burst.

In both Houses, members derided the South Sea Company directors as fraudsters and villains. Since so many parliamentarians had, themselves, helped the scheme, wittingly and unwittingly, they concealed their involvement through speeches laden with invective. They assumed the appropriate expressions of horror and spoke of the great injuries done to the people.

It was not all sham. Plenty of politicians had been taken in and made destitute.

Dublin-born writer and satirist Jonathan Swift, himself an early South Sea Company investor, wrote a 1721 poem about the collapse, referring in the piece to the miserable scenes near Garraway’s Coffee House. The first stanza follows:

“There is a gulf where thousands fell,

Here all the bold adventurers came;

A narrow sound, though deep as hell—

Change Alley is the dreadful name.”

The King returned from Germany. In 1721, he chose Robert Walpole to handle the crisis. Walpole was simultaneously appointed Leader of the House of Commons, First Lord of the Treasury and Chancellor of the Exchequer. Although a moderate who’d enhanced his fortunes by buying shares, he’d warned others against doing the same.

Walpole assented to the calls for reprisals. His deft response restored confidence in the economy. Walpole took money from certain South Sea Company directors, who’d grown exceptionally wealthy, leaving them with £10,000 (equivalent to £1.8 million in 2024). Blunt was the exception and allowed to keep only half that amount. The money was distributed to victims. Interrogated as part of the secret proceedings, Blunt’s memory conveniently failed him. He showed deference to the House, but revealed little.

Walpole’s Whig-led parliamentary investigation revealed the detail of the South Sea Company’s corruption. (Source: University Archives.)

While some participants had to be sacrificed, Walpole protected the royals. He did the same for the King’s mistresses, many of whom were involved or had foreknowledge of the crash.

Walpole’s actions reinforced the sovereign’s loyalty, shielded the court from public anger, and furthered his authority. The public saw him as the man who’d saved Great Britain. He held his three appointed positions for twenty years, and until his resignation was the most important minister in the House of Commons. Because of his power, he was sometimes called the chief minister or even the prime minister, but he repudiated that term. He was, he said, the servant of the King. Today, he is considered the first Prime Minister, although that position would not be formalised until 1885.

The last South Sea Company shares, which by 1722 had tumbled to their original price, were divided between the company’s two greatest rivals, the East India Company and the Bank of England. Remarkably, the South Sea Company remained in operation, though forced to sell most of its assets to the Spanish. It continued managing a portion of the national debt until 1853 when it was dissolved.

A composite image in part of the narrow Change Alley network as it appears today. At front is where Garraway’s stood. Atop is a stone engraving that reads ‘The Site of Garraway’s Coffee House Rebuilt 1874’. Jonathan’s is not visible in this image, but was less than 30 metres (100 feet) away, and its memorial plaque is shown at the top right.

Jonathan’s Coffee-House burned down in the Cornhill fire of 1748, which destroyed most of the area. It was rebuilt, but in 1773 the owners moved to a new site, which today is the London Stock Exchange. Garraway’s Coffee House too burned in the 1748 fire, was rebuilt, and operated until 1874 when it was demolished. A stone building now occupies the original location.

Modern Echoes, Warnings and Lessons

Three centuries after the South Sea Bubble, modern bubbles echo the same patterns of mania and deceit. The pattern is remarkably consistent: a grand narrative of transformative opportunity, prominent figures lending credibility, and the promise of wealth “hereafter to be promulgated.”

When cryptocurrency exchange FTX collapsed in 2022, it revealed the same fundamental truth that undid the South Sea Company – it was all flash and no substance. Enron is another echo of the South Sea Bubble, with the same political involvement, the same style of corruption and the same obfuscation. Enron executives routinely cooked their books, just as Blunt and the other South Sea Company managers did.

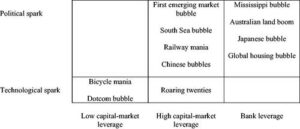

Table categorising historic economic bubbles by their spark—political or technological—and the type of leverage involved. (Source: Quinn, William & Turner, John D. (2020). Boom and Bust: A Global History of Financial Bubbles. Cambridge University Press.)

From WorldCom to Theranos, from govWorks to Wirecard, from dot-com darlings to fintech unicorns, modern markets have their own versions of the “company for carrying on an undertaking of great advantage, but nobody to know what it is.” The methods have evolved, but the underlying psychology remains unchanged. Today’s bubble companies don’t need coffee houses in Exchange Alley; they have online influencers and slick digital marketing campaigns.

Companies with opaque business models and overinflated valuations prey on what Charles Mackay called, in 1841, investors’ “thirst for gain”. The slow, sure profits of careful industry are despised. The modern bubble companies spread, as Pope wrote after the South Sea Bubble burst, “like a low-born mist”, and bring their investors and stakeholders to rapid decay. One day, they’re everywhere, the next, they’re gone.

Thrive by Sober Rules

The parallels between the South Sea Bubble and modern commercial obsessions are not just historical curiosities, or coincidences. The parallels show how to avoid similar risks today. Just as 18th-century investors might have saved themselves by questioning the South Sea Company’s actual trading prospects, modern businesses can protect themselves through diligent research and available precautions.

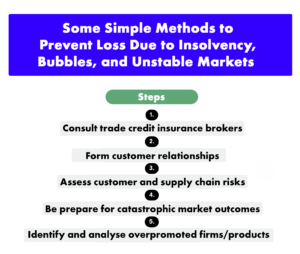

Adapted infographic on methods to mitigate risks from insolvency, bubbles, and unstable markets, inspired by iDenfy’s recommendations. (Adapted from iDenfy. Original concepts restructured for clarity and visual impact.)

In this era, critical thinking is more vital than ever. Investors must ask themselves whether they believe in a company’s potential or simply want to believe in it. Scrutinising financial statements, understanding business models, reading, investigating and considering worst-case scenarios can help individuals and businesses avoid failure.

For businesses engaged in trade, the importance of due diligence cannot be overstated. Trade credit insurance protects against the financial instability of partners and clients, ensuring resilience in uncertain times. Just as the South Sea Bubble shattered the British economy, modern business failures always ripple outwards, swallowing suppliers in debt and litigation. Protecting against such risks should be a matter of course. The available tools are simple, informative and practical, but most of all, they are essential.

The last stanza of Ned Ward’s verse, written 300 years ago, poignantly illustrates the folly of disconnected financial markets, a theme as relevant today as it was over three centuries ago.